Buyer Tools

Buyer Guide

Understanding APR - The total cost of your loan, including interest and certain fees, expressed as a yearly rate.

Down payments - The upfront amount you pay toward the home purchase, typically a percentage of the price.

Inspection costs - Fees for a professional evaluation of the property’s condition before purchase.

Appraisal fees - The cost of determining the home’s market value, usually required by lenders.

Escrow basics - A process where a third party holds funds and documents until all conditions of the sale are met.

Loan Insights

Fixed-rate - A loan with an interest rate that stays the same for the entire term.

Rate lock - An agreement that secures your interest rate for a set period while your loan is processed

PMI - Insurance required on some loans when the down payment is below a certain percentage.

FHA vs Conventional - Two common loan types with different requirements for credit, down payment, and insurance.

Refinance - Replacing your current loan with a new one to change your rate, term, or monthly payment.

Local Tax

Transfer tax rates - Taxes charged by state or local governments when a property changes ownership.

Title insurance - Protection against issues with the property’s ownership or legal claims.

Recording fees - Fees paid to officially record property documents with the local government.

Property tax prepay - Advance payment of property taxes collected at closing.

Attorney fees - Costs for legal services related to reviewing and completing the transaction.

What Are Closing Costs?

Closing costs are the fees and expenses paid at the end of a home purchase or refinance transaction. These costs are separate from the home’s purchase price and are usually paid at the closing table when ownership of the property officially transfers. Closing costs may include lender fees, title fees, appraisal fees, recording fees, government taxes, prepaid homeowners insurance, prepaid property taxes, escrow deposits, and other settlement-related charges.

For many home buyers, closing costs can be one of the most confusing parts of the transaction because they are made up of several smaller charges instead of one simple fee. Some fees are connected to the mortgage loan, such as underwriting, processing, discount points, credit report fees, and lender-related charges. Other fees are connected to the property transfer, such as title insurance, settlement services, recording fees, transfer taxes, and government filing costs.

Closing costs are not the same in every state, county, city, lender, or transaction. The final amount can change depending on the purchase price, loan amount, loan type, title company, local taxes, insurance requirements, escrow setup, seller credits, and market conditions.

Before closing, buyers typically receive a Loan Estimate and later a Closing Disclosure. These documents provide a more detailed breakdown of the estimated and final costs connected to the loan and transaction.

ClosingCosts4U is designed to help buyers estimate these expenses early so they can plan with more confidence. However, the numbers provided by this tool are for informational purposes only. Actual closing costs may vary and should always be confirmed with the lender, title company, settlement agent, or qualified professional handling the transaction.

What Is Cash to Close?

Cash to close is the total is the amount of money a home buyer must bring to the closing table in order to complete the purchase of a property. This amount includes the down payment, closing costs, prepaid expenses, escrow deposits, and any remaining fees required to finalize the transaction.

Many buyers confuse cash to close with closing costs, but they are not the same thing. Closing costs are only one part of the total cash needed at closing. Cash to close combines multiple financial components into one final amount.

The final cash to close amount can vary depending on several factors, including the purchase price, loan amount, loan type, interest rate, property taxes, homeowners insurance, escrow setup, prepaid interest, and seller credits. If the seller agrees to contribute toward closing costs, the buyer’s total cash to close may decrease.

Mortgage lenders usually provide an estimated cash to close amount on the Loan Estimate early in the mortgage process. Later, a final amount is provided on the Closing Disclosure before the transaction officially closes.

Understanding your estimated cash to close amount is important because it helps buyers prepare financially and avoid unexpected surprises before closing day. Buyers should always review their Loan Estimate and Closing Disclosure carefully and verify all numbers with their lender or settlement agent.

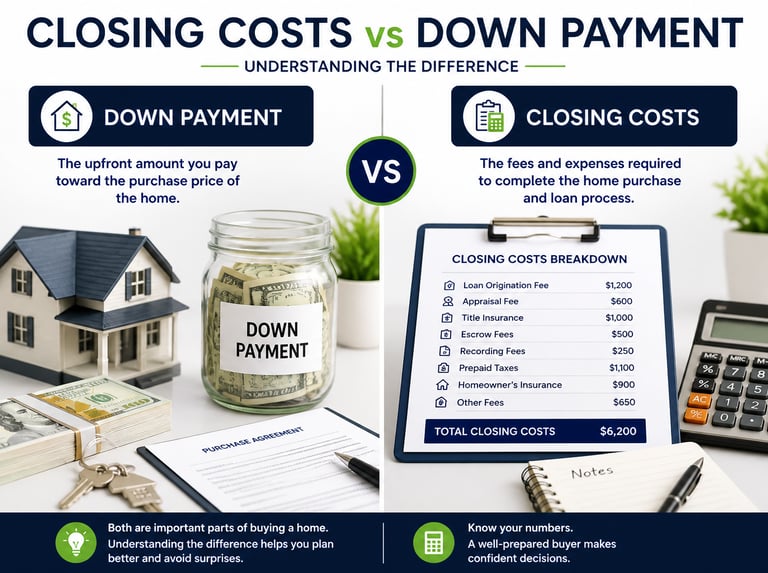

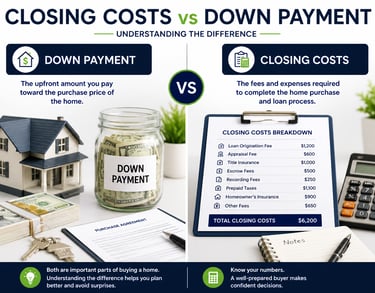

What Is the Difference Between Closing Costs and Down Payment?

Closing costs and down payment are both important parts of buying a home, but they are not the same thing.

A down payment is the portion of the home’s purchase price that the buyer pays upfront. The remaining balance is usually financed through a mortgage loan. For example, if a buyer purchases a $350,000 home with a 20% down payment, the buyer would pay $70,000 upfront while the remaining amount would be financed.

Closing costs are different because they are the fees and expenses associated with completing the real estate transaction and mortgage loan process. These costs may include lender fees, appraisal fees, title fees, escrow fees, recording fees, prepaid taxes, homeowners insurance, and other settlement-related charges.

Many home buyers mistakenly believe that the down payment covers all upfront costs, but buyers usually need additional money for closing costs and prepaid expenses. This is why understanding your estimated cash to close amount is extremely important before finalizing a home purchase.

The amount required for closing costs may vary depending on the state, lender, loan type, property taxes, insurance costs, escrow requirements, and local government fees. Some buyers may receive seller credits that help reduce their out-of-pocket closing costs, but these credits usually do not replace the required down payment.

Understanding the difference between closing costs and down payment helps buyers better prepare financially, avoid surprises during the closing process, and make more informed home-buying decisions.

What Home Buyers Are Saying

See how our tools are helping home buyers plan their closing costs with confidence.

Professional and easy to use. I finally understood where my money was going during the escrow period. These resources are invaluable for navigating the fintech space.

Marcus Reed

The calculator was spot on! It made planning my cash-to-close so much easier. I finally felt in control of my home buying process. Highly recommend this for any buyer.

Sarah Jensen